Last month in markets

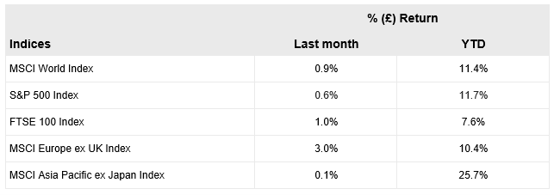

- Global equities (as measured by the MSCI World Index) were broadly flat over the month, albeit some strength in the US dollar led to a mildly positive return for sterling-based investors.

- The S&P 500 ended the month down in local currency terms, seemingly driven by profit taking in technology and AI-related stocks rather than any clear fundamental reason. ‘Value’ sectors and mid and smaller companies proved more resilient.

- The Q2 earnings growth expectations in the US remains very positive (above 20%) with the reporting season due to begin in a couple of weeks’ time. The positive earnings momentum in the technology sector is expected to continue, however there is strength across the market with other sectors such as energy and materials also expected to produce strong results, as they did in Q1.

- The oil price continued to fall sharply over the month as progress was made between the US and Iran to de-escalate the conflict and reopen the Strait of Hormuz. This easing in tensions lowered interest rate expectations and provided a leg of support to equity markets, particularly across Europe.

- The Japanese market also continued to perform well and, as expected, the Bank of Japan raised rates against a backdrop of strong wage growth and increasing goods inflation. Evidence is growing that the stimulus measures being introduced by Prime Minister Sanae Takaichi are impacting positively while the market continues to benefit from corporate reform, placing greater emphasis on releasing value to shareholders.

- As was expected, the European Central Bank also hiked rates, taking the deposit rate to 2.25%, despite inflation expectations falling over the month and mixed economic data.

- In the US, data continues to show that business activity is improving – the flash composite Purchasing Managers’ Index (‘PMI’) rose to 52.2, its highest level for five months, while higher energy prices are also pushing inflation higher (up to 4.2% year on year). Against this backdrop, the US Federal Reserve voted to keep rates on hold at its June meeting however the US dollar strengthened on the back of more hawkish rhetoric from the new Chair, Kevin Warsh, and a higher overall committee ‘dot plot’ indicating higher rate expectations. Markets are now pricing in two potential 25 basis point rate hikes in the US over next few months although there is a wide dispersion of views given all the uncertainties.

- Market reaction to the resignation of UK Prime Minister Keir Starmer was relatively muted. The UK government bond curve is slightly steeper than comparable yield curves in the US or Germany but remains far less steep than it is in France or Italy, implying that the market does not currently anticipate a dramatic deterioration in fiscal discipline from the new leader (widely expected to be Andy Burnham). Markets also seem increasingly of the view that the impact of lower energy prices, and a softer labour market, will mean that the Bank of England does not elect to raise rates in response to a shorter-term, energy-price-led spike in inflation.

Equities

10-year government bond yields

Currencies

Source: FactSet and Morningstar as at 30 June 2026. Past performance is not a guide to future results.

For a detailed overview of market developments during the second quarter and our current portfolio positioning, please read our Q2 Investment Review. For more information about Bordier UK or our services, please contact a member of our team.

This page is issued and approved by Bordier & Cie (UK) PLC (‘Bordier UK’). Incorporated in England No: 1583393, registered address 23 King Street, St James’s, London, SW1Y 6QY. The company is authorised and regulated by the Financial Conduct Authority (‘FCA’).

Bordier UK is a wealth and investment manager dedicated to providing portfolio management services. We offer Restricted advice as defined by the FCA, which means that if we make a personal recommendation of an investment solution to you, it will be from Bordier UK’s range of investment propositions and will reflect your needs and your approach to risk.

This page is not intended as an offer to acquire or dispose of any security or interest in any security. Potential investors should take their own independent advice to assess the suitability of investments. Whilst every effort has been made to ensure that the information contained in this page is correct, the directors of Bordier UK can take no responsibility for any action taken (or not taken) as a result of the matters discussed within it.