Iran war – markets respond to threat of higher inflation but yet to show much concern over potentially weaker growth

Bond markets

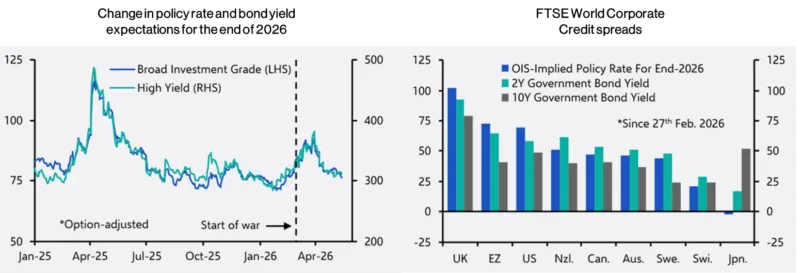

There has been a quite dramatic increase in interest rate and bond yield expectations since the start of the Iran war, with the most notable shift in the UK (as demonstrated by the left-hand chart below). As such, inflation concerns are clearly apparent, and rate hikes are now priced into bond markets across much of the developed world.

Within the corporate bond universe, credit spreads did initially spike when the war began but have since fallen below pre-spike levels (see right-hand chart below), suggesting limited concerns over the prospect of weaker growth stemming from the impact of the war.

Source: LSEG and Capital Economics as at 14 May 2026.

Equity markets

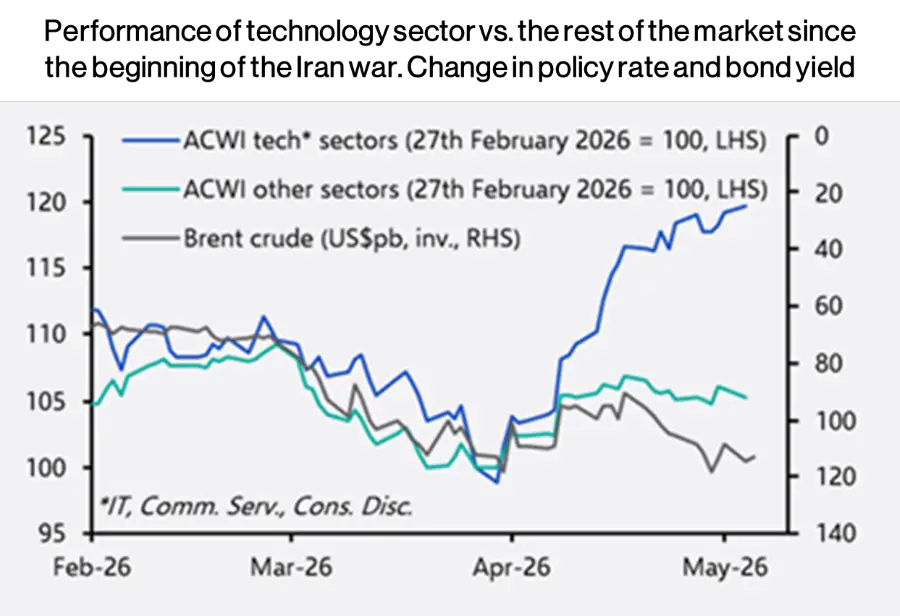

After falling heavily in March, equity markets have recovered strongly with the technology sector, and semi-conductor companies in particular, a key driver.

Source: LSEG and Capital Economics as at 18 May 2026.

Somewhat surprisingly, given the still uncertain situation in the Middle East, the equity ‘risk premium’ (as measured by the forward 12-month earnings yield of the S&P 500 Index minus the 10-year TIPs yield) has actually fallen slightly since the beginning of the war.

What should we infer from this?

Market movements since the beginning of April suggest that overall expectations are still for some shorter-term resolution to the conflict that brings some easing in energy prices and limits potential economic damage. This also remains our base case. If we do see some reopening in the Strait of Hormuz in the next few weeks, then we still believe there is potential for a further rally in equities (especially outside technology) and also some recovery in bonds.

Given the seemingly entrenched current position with regards to the conflict we should, however, expect some market volatility as expectations on its path oscillate. The longer the conflict continues the more we would expect markets to start pricing in the potential impact on economic growth, with clear implications for equity and credit markets. If expectations did then turn more towards recessionary conditions, we would also likely see sovereign bond behaviour reverse and see yields start to fall as growth concerns worsened. Clearly in this (worsening) conflict scenario changes to our asset allocation and positioning might be required.

This page is issued and approved by Bordier & Cie (UK) PLC (‘Bordier UK’). Incorporated in England No: 1583393, registered address 23 King Street, St James’s, London, SW1Y 6QY. The company is authorised and regulated by the Financial Conduct Authority (‘FCA’).

Bordier UK is a specialist investment manager dedicated to providing portfolio management services. We offer Restricted advice as defined by the FCA, which means that if we make a personal recommendation of an investment solution to you, it will be from Bordier UK’s range of investment propositions and will reflect your needs and your approach to risk.

This page is not intended as an offer to acquire or dispose of any security or interest in any security. Potential investors should take their own independent advice to assess the suitability of investments. Whilst every effort has been made to ensure that the information contained in this page is correct, the directors of Bordier UK can take no responsibility for any action taken (or not taken) as a result of the matters discussed within it.